A failure in a bank’s data centre cooling system can cascade into significant operational disruptions. Transactions are halted, client applications are delayed, and financial impacts begin to mount. This type of event may seem isolated at first glance, but its effects quickly multiply as various interconnected parameters come into play—downtime, transaction volumes, and the probability of data corruption, among others.

To effectively manage such scenarios, decision-makers must understand how these factors interact to drive financial consequences. Simulations provide a critical tool for analysing these complex relationships, allowing organisations to prepare for uncertainties and ensure resilience.

Unpacking the Interconnected Costs

When systems go offline, the cost isn’t driven by a single factor but by a web of interrelated parameters. In this case, a cooling system failure impacts the bank’s ability to process loan transactions, creating a domino effect across multiple dimensions:

1. Transaction Backlogs Multiply the Operational Impact At an average rate of 100 transactions per hour, downtime leads to a growing backlog. With recovery times typically spanning six hours, over 600 transactions are delayed in most scenarios. In extreme cases, this backlog could exceed 1,200 transactions. These backlogs are more than operational delays—they drive revenue losses and increase the likelihood of customer dissatisfaction.

2. Revenue Loss Escalates with Downtime Each delayed loan transaction represents missed revenue opportunities. At an average loss of £400 per transaction, the total revenue impact scales with the backlog. Simulations show average losses of £243,000, with the potential to reach over £500,000 in severe cases. This demonstrates the financial sensitivity of high-value services like loan processing.

3. Data Corruption Adds Complexity to Recovery A 25% chance of data corruption introduces additional uncertainty. Restoring corrupted data is costly, with an average hourly restoration cost of £5,000 and a mean restoration time of four hours.

4. Client Compensation Reflects Reputation Management Delays in loan processing lead to customer dissatisfaction, which institutions often address through compensation. With an average compensation of £100 per transaction, the total cost of appeasing impacted clients is approximately £60,600 in most cases. Although smaller than the revenue impact, these costs highlight the reputational stakes tied to operational resilience.

The total financial impact, when all factors are combined, averages £308,000. However, the simulation shows that in extreme cases, this figure can exceed £600,000, underscoring the need to plan for both typical and outlier events.

Insights for Decision-Making

The value of simulations lies in their ability to capture the interconnected nature of risks. Each parameter—whether it’s incident duration or the probability of data corruption—doesn’t exist in isolation but influences the broader financial picture.

For senior management, these insights are invaluable. They highlight where vulnerabilities exist, quantify the potential costs of operational failures, and provide a basis for robust decision-making. For instance, understanding that revenue losses scale exponentially with downtime emphasises the importance of investing in rapid recovery systems. Similarly, the significant but less predictable costs tied to data corruption might justify enhanced safeguards for data integrity.

When discussing model risk in financial services, conversations often gravitate toward trading algorithms or credit scoring models. However, some of the most significant model risks lurk in longer-term business activities where validation is challenging and errors compound over years. Today, we’ll explore one such scenario through a Monte Carlo simulation of a model failure at a hypothetical specialist insurer.

Setting the Scene: A Specialist Insurance Provider

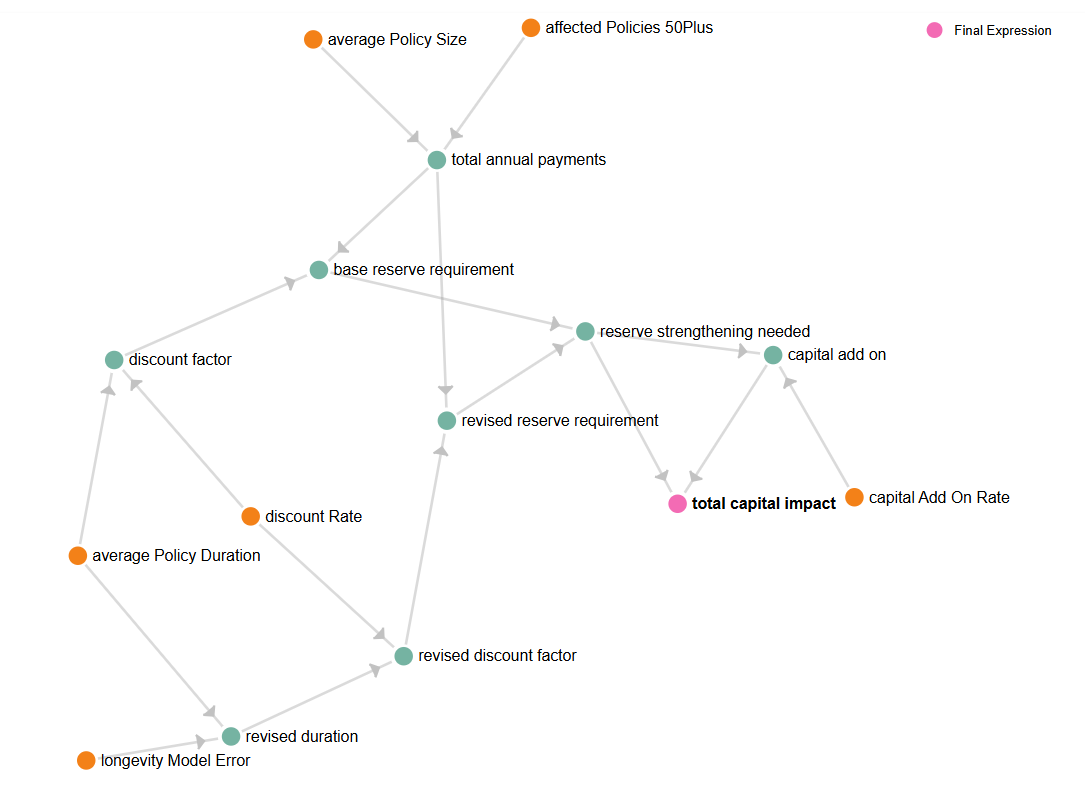

Our case study focuses on a UK-based specialist insurer catering exclusively to high-net-worth (HNW) individuals. The firm’s unique selling proposition centres on sophisticated underwriting and bespoke pension products, particularly targeting individuals with investable assets exceeding £5 million. With approximately 400 policies on their books and average annual payments of £250,000 per policy, they manage around £100 million in annual payments – a small but focused operation in the insurance landscape.

The Model Risk Scenario

The trigger event in our simulation is the discovery of a systematic underestimation in the firm’s longevity predictions for their HNW client base. The model failed to adequately capture several crucial factors affecting wealthy individuals’ life expectancy: superior access to healthcare, early adoption of life-extending treatments, and lifestyle factors specific to the HNW segment. This isn’t merely an academic concern – it directly affects the reserves needed to meet future obligations.

Understanding the Portfolio Characteristics

The simulation examines a portfolio of around 300 policies for clients aged 50 and above. These aren’t ordinary pension policies – with average annual payments of £250,000, they represent significant long-term commitments to wealthy individuals expecting premium service. The portfolio’s duration averages 25 years, reflecting the long-term nature of pension obligations and the relatively younger age profile of the affected clients.

Technical Impact: The Numbers Behind the Crisis

The core of our simulation revolves around the longevity model error, estimated at 15% on average. This means the model has been systematically underestimating how long clients are likely to live by about 15%. For a pension provider, this translates directly into longer payment periods and, consequently, larger reserve requirements.

The simulation calculates reserve requirements using a simplified discount rate approach, averaging 2%. This helps convert future payment obligations into today’s monetary terms. The base reserve requirement – the amount needed before discovering the model error – averages £1.47 billion. This figure makes sense given the annual payment obligations and the long-term nature of the commitments.

The Capital Impact

When the model error is discovered, two immediate financial impacts emerge. First, the firm needs to strengthen its reserves by approximately £161 million to account for the longer expected payment period. Second, regulators typically require additional capital (a “capital add-on”) as a buffer against uncertainty, simulated at around £24 million.

The total capital impact, averaging £187 million, represents a severe but plausible shock for an insurer of this size. To put this in perspective, it’s roughly 2.5 times the annual premium income – a significant hit that would require urgent management attention but shouldn’t necessarily be fatal to a well-capitalised specialist insurer.

Regulatory Implications

The simulation includes stress testing at levels relevant for regulatory reporting. The 1-in-20 and 1-in-200 scenarios, representing 95th and 99.5th percentiles respectively, help understand the potential severity under stressed conditions. These metrics are particularly important for the Own Risk and Solvency Assessment (ORSA) process required by insurance regulators.

The regulatory response would likely extend beyond just capital requirements. The nature of the error – systematic underestimation of longevity in a firm marketing itself on sophisticated underwriting – could trigger enhanced supervision and potentially a skilled persons review under Section 166 of the Financial Services and Markets Act.

Monte Carlo Simulation Approach

The simulation employs Monte Carlo methods to model uncertainty in key parameters. Rather than using single-point estimates, we allow each parameter to vary according to specified probability distributions. This provides a more nuanced understanding of possible outcomes and their likelihood.

Key parameters include the number of affected policies, average policy size, policy duration, and the magnitude of the longevity model error. The simulation also incorporates a discount rate to properly value future cash flows. By running thousands of iterations with different combinations of these parameters, we build a comprehensive picture of potential impacts.

Interpreting the Results

The simulation results demonstrate several interesting features. The distribution of outcomes shows a clear rightward skew in the total capital impact, meaning extreme adverse scenarios are more likely than extremely favorable ones. This asymmetry makes sense given the compounding nature of longevity risk.

The mean total capital impact of £187 million represents a severe but credible scenario for a specialist insurer. It’s large enough to require significant management action – possibly including capital raising – but not so large as to be implausible for a firm of this size and specialisation.

Limitations and Considerations

While the Monte Carlo simulation provides valuable insights into the potential impact of model risk on our hypothetical specialist insurer, it’s important to acknowledge the limitations inherent in this first-pass assessment. Recognising these limitations not only adds transparency but also highlights areas for further refinement and analysis.

Magnitude of Longevity Underestimation: The simulation assumes a 15% systematic underestimation of life expectancy among high-net-worth (HNW) clients. This significant margin was deliberately chosen to illustrate the potential impact of model errors. In reality, such a substantial oversight would likely stem from multiple factors, including outdated mortality tables, failure to account for medical advancements, or misclassification of client health profiles. While plausible, this assumption underscores the need for models to be continuously updated and validated against emerging data.

Portfolio Characteristics: We assumed that 300 out of 400 policies belong to clients aged 50 and above, with an average annual payment of £250,000 per policy. These figures are estimates meant to represent a typical portfolio for a specialist insurer in the HNW segment. However, actual client demographics and policy details may vary, and more granular data would enhance the accuracy of the simulation.

Discount Rate Selection: A constant discount rate of 2% was used to calculate the present value of future payment obligations. This simplified approach doesn’t account for potential fluctuations in interest rates, inflation, or changes in the economic environment over the 25-year average policy duration. A sensitivity analysis using a range of discount rates could provide a more robust understanding of the reserve requirements under different economic scenarios.

Broader Implications for Risk Management

This case study highlights several crucial aspects of model risk management. First, model errors in long-term business can create significant exposures before detection. Second, specialist firms marketing themselves on technical expertise face amplified reputational risks from model failures. Finally, the interaction between technical errors and regulatory requirements can create compound impacts on capital.

For risk professionals outside the insurance sector, the principle remains relevant: models driving long-term business decisions require particularly robust validation and governance. The impact of model errors compounds over time, and detection may come too late for simple remediation.

The simulation also demonstrates how quantitative techniques can help risk managers understand complex scenarios. While the specific numbers matter, the real value lies in understanding the relationships between different factors and how they combine to create overall impact. This structured approach to scenario analysis can be applied across various risk types and business contexts.

Remember, while this scenario is hypothetical, it’s grounded in realistic parameters and industry experience. Similar model failures have occurred across financial services, often with comparable relative impacts. The key lesson isn’t about the specific numbers but about the importance of robust model governance, particularly for models driving long-term business decisions.

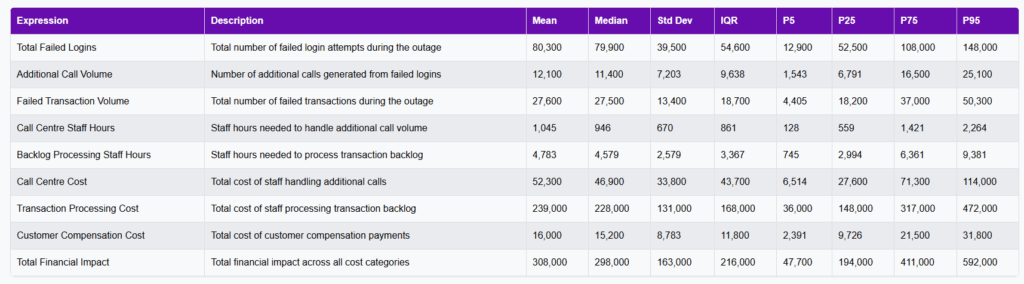

Inside a One-Hour Outage: Monte Carlo Simulation Reveals Risks and Resilience

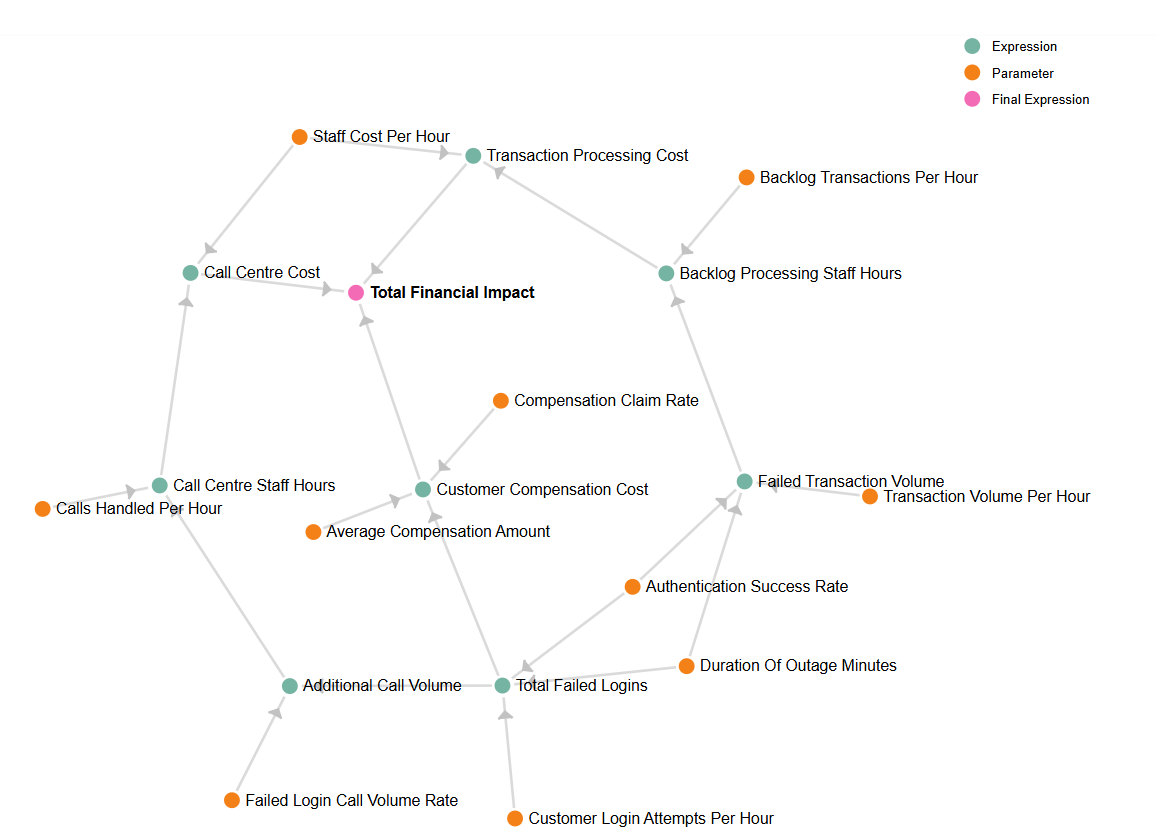

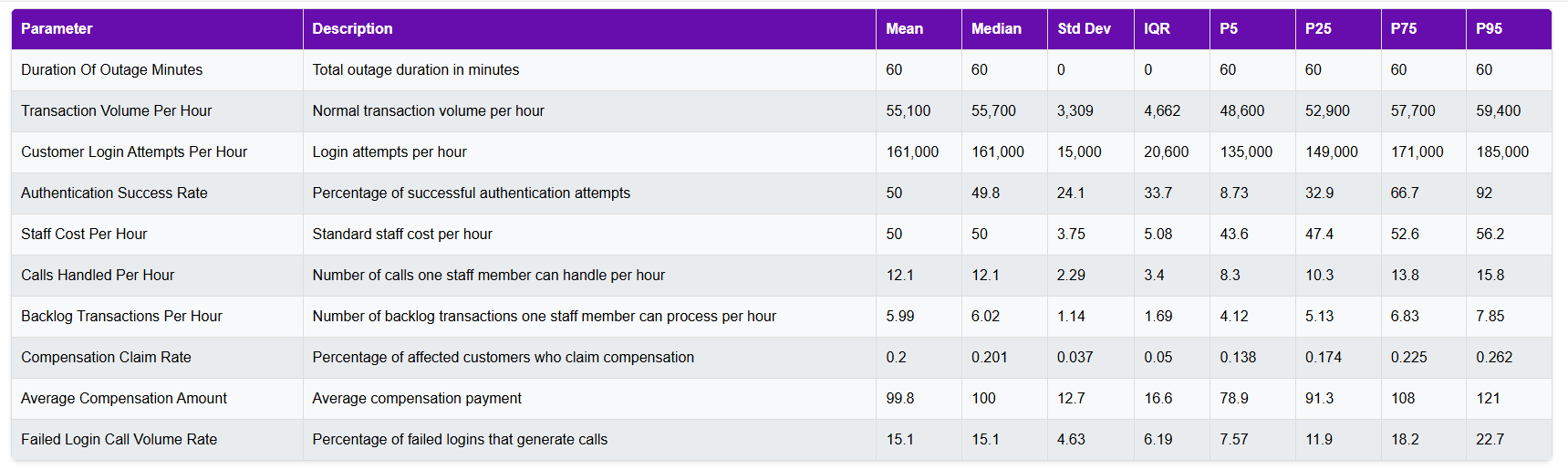

Imagine it’s 9:15 on a bustling Tuesday morning at a mid-sized UK bank with £70 billion in assets. As employees settle into their tasks and customers log into their accounts, disaster strikes: the bank’s Identity and Access Management (IAM) system fails entirely. For the next hour, neither customers nor staff can authenticate into digital banking systems. This unexpected outage locks out 2 million customers and 12,000 employees, halting services that are vital to the bank’s day-to-day operations. While the issue lasts only an hour, the effects are anything but brief.

To understand the full scope of this risk, we used a Monte Carlo simulation to model thousands of potential outcomes based on real-world parameters. By doing so, the bank could quantify the impact of this one-hour outage across financial, operational, and customer service dimensions. This simulation reveals important insights into how an hour of downtime can cascade across an organisation, emphasising the importance of robust planning, both for restoring services and for managing the downstream effects.

Financial Impact: Gauging the True Cost of Downtime

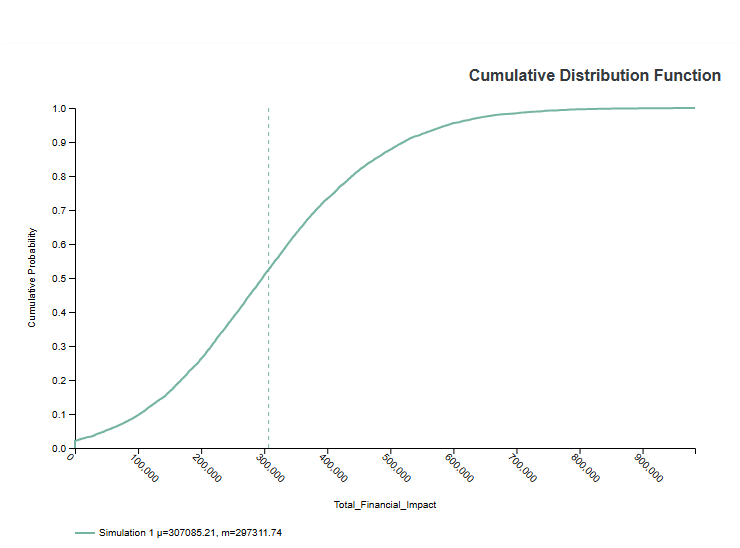

When IAM services fail, a bank’s financial exposure goes beyond immediate technical recovery costs. The simulation shows that on average financial losses would be around £300,000. This figure is derived from multiple sources of cost, including call center staffing, transaction backlog processing, and customer compensation payments. There is a unlikely scenario, one-in-20 outcomes, that the financial impact could reach £600,000, and for an even more extreme scenario — the financial impact exceeding £900,000 — the probability drops to 0.5%, equivalent to a 1-in-200 event. These probabilities give the bank perspective on the severity of the risk and highlight the need for preventative measures, such as investing in IAM system reliability and backup solutions.

The primary driver of these costs is the volume of failed login attempts and subsequent customer support calls. During the outage, the bank would experience an estimated 80,000 login attempts per hour. With authentication completely disabled, all these attempts would fail, which leads directly into the next area of impact: customer support.

Customer Service Strain: Handling a Surge in Support Requests

Failed logins not only disrupt customer access but also create a cascade effect on the bank’s customer service resources. The model indicates that a large proportion of these failed logins would result in calls to the bank’s support center, especially as customers become frustrated with their inability to access accounts. According to the simulation, around 15% of failed login attempts are likely to generate a support call, resulting in over 12,000 additional calls during the outage. This sudden spike in call volume would require substantial staffing adjustments, potentially needing hundreds of additional call center hours just to handle the influx.

The model further estimates that the total number of call center staff hours required to meet this spike in demand would exceed 1000 hours. Without proper preparation, customers would face long wait times, leading to frustration and potential reputational damage. This underscores the need for banks to have flexible, surge-ready call center resources. Contingency planning for high-impact outages should consider not only the technical recovery process but also the ability to respond to customer needs in real-time, maintaining service standards in stressed conditions.

Operational Strain: Clearing the Transaction Backlog

An IAM outage also disrupts the bank’s internal operations, especially around transaction processing. With digital services offline, standard banking transactions—payments, transfers, deposits—are interrupted. The simulation reveals that every hour of disruption leaves behind a significant backlog of failed transactions, each requiring manual intervention to clear once the systems are back online.

In this scenario, the estimated backlog of failed transactions, based on normal transaction volumes of 50,000 per hour, is substantial and the simulation projects that clearing this backlog would require extensive staffing and add considerable operational costs. The burden of clearing transaction backlogs can persist for hours or even days after the initial outage, impacting productivity and workflow. This highlights the importance of having a rapid post-outage recovery plan, with processes in place to prioritise and address transaction backlogs efficiently.

Deeper Exploration of Financial Drivers in the IAM Outage

When considering the financial impact of a one-hour IAM outage, it’s helpful to break down the specific cost drivers involved, as each component plays a distinct role in the total potential loss. According to the Monte Carlo simulation, the main contributors to the financial impact include:

Call Center Costs: The surge in customer service calls resulting from failed logins is one of the largest direct costs. With an estimated 10,000 additional calls generated during the outage, the bank would need to deploy significant resources to handle the increased call volume. Staffing costs for the additional call center hours needed are projected to contribute substantially to the overall financial impact. If the bank is unable to quickly adjust staffing, these costs could rise even higher as wait times increase and customer satisfaction declines.

Transaction Processing Costs: Each failed transaction that occurs during the outage contributes to a backlog, requiring manual processing once systems are back online. In the scenario modeled, backlog processing would necessitate considerable staff hours, adding operational costs that extend beyond the outage itself. Since each staff member can only handle a limited number of backlog transactions per hour, this cost can scale quickly, especially if the backlog disrupts the bank’s regular transaction flow.

Customer Compensation Costs: The simulation estimates that around 0.1% of affected customers could file compensation claims due to the inconvenience or financial loss experienced during the outage. While this percentage seems small, it represents roughly 2,100 claims for a customer base of 2 million, with each payout averaging £50. While this may not be a primary driver, customer compensation remains a meaningful cost that can add up quickly, especially when considering both direct payouts and the administrative resources required to handle claims.

Together, these components—call center staffing, transaction backlog processing, and customer compensation—form a complex web of costs that the bank would need to address in an actual outage scenario. Understanding the breakdown allows the bank to focus its contingency planning on areas with the highest impact, ensuring that resources are allocated to the most pressing financial and operational needs during a crisis.

Beyond the Numbers: Strategic Insights for Risk Management

The insights from this simulation aren’t just theoretical; they provide actionable guidance for the bank’s risk management strategy. By analysing financial, operational, and customer service impacts, the bank can make more informed decisions on how to prepare for, mitigate, and respond to an IAM service outage.

First, the data highlights the value of investing in system redundancy and reliability for IAM services. Given the relatively low but substantial risk of severe financial impact, allocating resources to prevent or quickly recover from IAM failures can provide a strong return on investment.

Second, the findings point to the need for flexible, surge-ready customer support teams. Ensuring that additional call center resources can be mobilised quickly during a crisis is essential to maintaining service levels and customer satisfaction.

Finally, the operational insights around transaction backlogs underscore the importance of having a dedicated post-outage recovery process. This includes clear prioritisation of backlog transactions, efficient staffing plans, and perhaps automated tools to streamline the manual process.

Enhancing Risk Mitigation: Practical Strategies to Reduce Impact

The Monte Carlo simulation results highlight the significant strain an IAM outage could place on financial, operational, and customer-facing functions. Based on these insights, the bank could explore several practical mitigation strategies to minimise both the likelihood and impact of a future IAM outage:

Investing in System Redundancy: One of the most direct ways to prevent outages is by enhancing IAM system resilience. Implementing redundancy measures, such as backup servers, automated failover systems, and diversified network paths, can help ensure continuity even if the primary IAM system encounters issues. Regular testing of these systems is essential to ensure they work seamlessly during a real incident.

Developing a Surge Staffing Plan for Call Centers: Given the likelihood of a call volume spike, the bank could create a contingency plan to deploy additional call center staff at short notice. This might include cross-training employees or establishing partnerships with third-party customer service providers. By having a flexible staffing strategy, the bank can ensure it meets customer demand during high-impact events without compromising response times.

Implementing Automated Backlog Processing Tools: The operational impact of clearing transaction backlogs can be minimised with automation. Robotic Process Automation (RPA) tools, for instance, can assist in processing transactions more quickly and efficiently, reducing the manual workload on staff. By automating repetitive transaction handling tasks, the bank can clear backlogs faster and limit the disruption to daily operations.

Establishing a Customer Communication Protocol: During an outage, proactive communication is crucial for maintaining customer trust. The bank should have in place a pre-planned communication protocol that includes regular updates on service status, expected recovery times, and instructions on alternative service options. Transparent communication can help reduce frustration and potentially lower the number of customer service calls and compensation claims, as customers are kept informed of the situation.

These mitigation strategies represent a proactive approach to managing the risks of an IAM outage. By addressing both technical and operational contingencies, the bank can enhance its resilience and better safeguard customer relationships and financial stability in the face of unforeseen disruptions.

The Broader Value of Monte Carlo Simulations in Financial Services

In a world increasingly driven by digital services, Monte Carlo simulations are becoming essential tools for operational resilience. They allow banks to anticipate the potential outcomes of rare but impactful events, giving them a clearer picture of risks and required responses. As this scenario shows, the power of simulations lies in their ability to break down complex, interconnected risks—financial, operational, and customer-related—into actionable insights.

By proactively modeling various scenarios, banks can develop targeted strategies to mitigate disruptions, enhance customer service, and maintain operational continuity. In a highly competitive market, where both customers and regulators expect uninterrupted access to financial services, simulation-based risk management is not just a defensive strategy—it’s a crucial component of building resilience and trust.

For financial institutions and other sectors facing complex operational risks, Monte Carlo simulations offer a pathway to understanding and preparing for the uncertainties that come with digital dependency. Through data-driven insights, organisations can strengthen their defenses, ensuring they’re not only reactive but also resilient when the unexpected occurs.

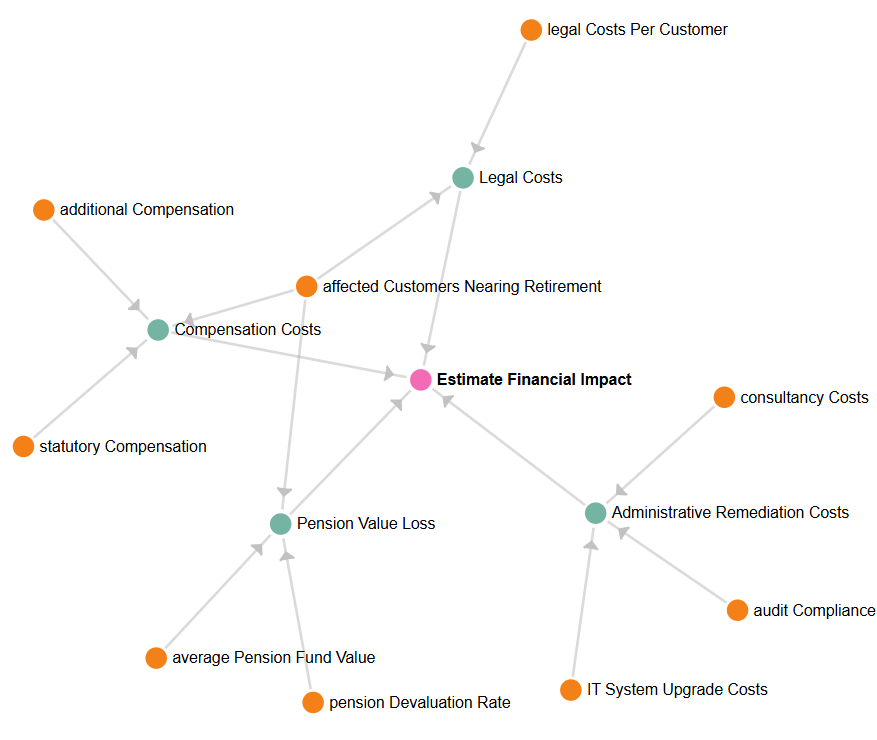

When a prominent UK bank acquired a pension fund division, it saw the acquisition as an opportunity to expand its reach and strengthen client relationships. However, in the transition, an aggressive investment strategy—allocating high-yield, high-risk assets into pension portfolios – was applied to a small cohort of clients: these were clients aged 50 and above who were nearing retirement and required stability over risk.

As market conditions shifted unfavourably, the investments declined, causing a sharp devaluation in the pension funds of affected clients. Though the number of impacted clients was relatively small, the potential financial consequences for both the bank and its clients could be substantial. This scenario examines how the bank can navigate multiple layers of financial and operational fallout, from compensating clients to defending against potential legal claims, all while overhauling internal controls to prevent a repeat incident.

To understand the scale and variability of this impact, we conducted a Monte Carlo simulation—running thousands of hypothetical scenarios to map out the potential range of financial outcomes. Here’s what the simulation revealed about the interconnected costs and risks that this oversight created.

Understanding the Drivers of Financial Exposure

At the core of this scenario are a few key drivers that amplify the financial and reputational risks for the bank:

High Devaluation of Client Pensions The small cohort of affected clients holds, on average, sizable pension funds. For these individuals, even minor percentage losses translate into significant amounts. The simulation shows that, given the aggressive investment allocation and volatile market conditions, the average potential loss across these clients could easily reach millions. Because these clients are close to retirement, the impact of this devaluation is especially painful, leading to both financial stress and a sense of betrayal, as these clients had trusted the bank to protect their retirement funds.

The Cost of Compensation In the UK, pension providers are subject to statutory compensation requirements, meaning the bank is legally obligated to offer a baseline level of reimbursement to affected clients. However, in this case, statutory compensation may not be enough. The bank’s need to manage client relationships and avoid mass discontent may lead to additional, discretionary compensation. For a small but financially significant client group, these combined costs quickly escalate, creating a hefty financial burden as the bank tries to repair its reputation and appease dissatisfied clients.

Legal Exposure and the Risk of Escalating Claims With clients who have suffered substantial personal financial losses, the risk of legal action is high. However, legal exposure here is unpredictable: not all clients may sue, but those who do could seek significant damages. Our simulation indicates that while most scenarios result in modest or negligible legal costs, a subset of cases shows the potential for high-impact lawsuits that could lead to steep legal expenses. This variability introduces an additional layer of financial uncertainty, as even a handful of high-profile claims could drive up costs dramatically.

Operational and Governance Remediation The crisis didn’t just expose issues in investment strategy; it revealed deeper weaknesses in the bank’s governance and risk oversight. To correct these systemic issues, the bank must now invest in costly remediation efforts, including IT system upgrades, compliance reviews, and governance restructuring. These costs, though necessary to prevent future mismanagement, add to the financial strain. According to the simulation, these administrative and operational costs alone can run into the hundreds of thousands, representing a proactive but costly attempt to rebuild robust internal controls.

The Monte Carlo Simulation: Mapping Financial Uncertainty

The Monte Carlo simulation was pivotal in showing just how volatile these outcomes could be. By modelling thousands of possible scenarios, the bank could see the distribution of financial impacts, from typical cases to rare but severe outcomes. The simulation highlighted two important insights:

A Broad Range of Possible Outcomes: The devaluation of pension funds, compensation, legal exposure, and remediation costs all varied widely, with some scenarios showing manageable costs while others suggested substantial financial strain. This range underscores the difficulty in predicting exact financial exposure when operational issues and client dissatisfaction are involved.

The Risk of Trigger Events: Certain discrete events—such as a major lawsuit or a regulatory fine—could amplify the bank’s exposure dramatically. While not every scenario includes these high-impact events, those that do significantly increase the financial burden. This insight underscores the importance of contingency planning and reinforces the need for a comprehensive, risk-aware approach to client fund management.

This scenario offers a cautionary tale: even a small client cohort, if financially significant, can create major exposure if risk management protocols are not integrated and enforced across all divisions. For the bank, this acquisition proved that aligning governance structures and oversight frameworks is critical, especially when absorbing a new business line with differing risk practices. Moving forward, the bank will need to ensure that investment strategies align with client profiles, particularly for clients nearing retirement who are far less tolerant of volatility.

By conducting this type of scenario analysis, the bank gains a clearer understanding of the full scope of financial, operational, and reputational risks. The results highlight the importance of proactive risk management, not just in client-facing decisions but in governance practices that safeguard client assets and maintain trust.

Over the weekend, TrustePensions implemented a routine update to their in-house pension management system, “PensionFlow.” On Monday morning, operations at their Birmingham headquarters resumed as usual, with client transactions processing through the system, allocating funds to various pension accounts. However, an untested piece of code was included in that update—a small oversight in the release process that would soon cause a significant issue.

Among the thousands of accounts managed by TrustePensions, approximately 100 were engaged in high-value transactions, including large pension withdrawals, annuity purchases, and mid-cycle contributions. These transactions require manual processing and additional layers of validation to ensure accuracy and compliance. The untested code inadvertently misallocated client funds across these 100 accounts.

By midday, a few clients had noticed discrepancies in their account balances. Initially, these anomalies were assumed to be routine market fluctuations, and customer service handled them accordingly. However, as the afternoon progressed and the end-of-day reconciliation began, the reconciliation team, led by Daniel Lewis, began noting the discrepancies. A detailed investigation revealed the misallocation caused by the weekend release, necessitating immediate action.

The response was swift: Simon Turner, the Chief Technology Officer, halted all new transactions and rolled back the update. Reprocessing the day’s transactions, verifying data accuracy, and restoring correct balances was a labor-intensive effort, extending well beyond normal operating hours. TrustePensions would have to suspend pension contributions and adjustments for the affected clients—potentially adding to the complexity of each reconciliation.

Compounding the challenge, there was a 20% chance that an additional cohort of clients—estimated between 50 to 100 accounts—might also require reconciliation, potentially increasing the workload. These accounts involved complex transactions that couldn’t be swiftly automated, necessitating manual intervention and increasing the risk of further errors.

Reconciliation: The Real Picture

For TrustePensions, a firm with a zero-tolerance policy on client money misallocations, the real challenge is not just how long reconciliation will take—but how quickly the issue can be resolved. The firm needs to know it is operationally resilient because, according to the Monte Carlo simulation, the total effort required to resolve the misallocation averages 15.6 days of work if handled by a single person.

The practical implication is that 16 staff members would need to be fully dedicated for an entire day to bring client accounts back in line. This raises critical questions: Does TrustePensions have the capacity to handle this in-house, or will they need to outsource the reconciliation effort? Internal teams may be stretched thin or lack the expertise needed to handle such a large, rapid reconciliation task.

This underscores the importance of resilience in effective risk management—not just estimating how long it may take to recover, but ensuring the right people, with the right skills, are available when needed.

Operational Resilience: A Board-Level Issue

In this scenario, the real challenge lies in resolving the issue within the firm’s zero-tolerance policy on client money misallocations. TrustePensions must immediately determine whether it has the internal capacity to redeploy staff or if external consultants need to be brought in—skilled, fast, and available on the same day—to ensure the issue is fully reconciled as soon as possible. Missing this deadline wouldn’t just breach internal thresholds—it would likely set off alarm bells with the FCA.

This is where the Key Risk Indicators (KRIs), tested through the scenario simulation, come into play. The KRI threshold isn’t just a nice-to-have—it’s an early-warning trigger. It tests whether the firm can mobilise sufficient, qualified resources to compress what would normally be a multi-week reconciliation process into a single day. This is not business as usual, and the Board must ensure that these KRIs serve as real action points—not hypothetical markers.

KRIs should prompt an immediate response whether triggered by live events or through plausible scenario simulations. The Board must shift its focus to ensuring that the firm’s operational resilience can meet the demands of these KRIs. The goal is simple: avoid breaching the trust of both clients and regulators by ensuring the firm is always ready to respond swiftly and effectively.

Financial Impact: Beyond Initial Estimates

The incident was projected to cost £15,600, based on the updated estimate of time and cost:

This projection assumes an average external resource rate of £2,000 per day, with each day covering an eight-hour shift. Reconciling 100 client accounts would take approximately 1 hour per account, or about 15.6 days in total.

However, the zero-tolerance policy makes this a far more complex operational challenge. Rather than spreading the workload across many days, the firm must concentrate the effort into a single day. Furthermore, the simulation has challenged a number of baseline assumptions, meaning the resulting analysis suggests the firm needs to effectively compress 15.6 days’ worth of work into just 24 hours.

The cost implications extend beyond just time. TrustePensions must determine whether it could pull in internal teams, which would strain other operations, or whether it could secure enough skilled external consultants to handle the volume of work. Either option will add significantly to the overall cost and bring their own risks. Based on our simulation, the financial impact is expected to be nearer £61,700, with the potential to reach £123,000 if additional cases are identified.

Beyond the ripple effect of operational risk costs due to urgency and skilled resourcing, this scenario reveals a key takeaway: what starts as an impact assessment of a client money misallocation can become a resilience testing opportunity. The significantly increased financial implications emphasise the need for TrustePensions to invest in advanced reconciliation tools, enhance staff training, and establish robust incident response protocols to effectively manage and mitigate such risks.

In banking, some risks are obvious—credit defaults, market downturns, or operational failures. Others are more subtle but equally impactful. The loss of a small, specialised team may seem manageable but, as our analysis shows, can trigger financial consequences extending beyond the immediate impact.

This article examines a scenario in which a bank loses its Credit Risk Modelling Team, leading to a gradual degradation of the accuracy of its credit models over 12 months. Using a Monte Carlo simulation, we quantify the potential financial impact of this event and explore the relationships between the various outcomes.

The Core Impact: Model Accuracy and Revenue Loss

Credit risk models are the engine behind the pricing and management of high-risk loan portfolios, such as commercial loans and subprime lending. In this simulation, a 5% reduction in model accuracy results in £125,000 in lost revenue from a £50 million portfolio over 12 months. This loss results from the bank’s struggle to price loans accurately—either being overly cautious and losing business or accepting riskier loans that may lead to future losses.

This revenue loss represents a 0.25% decline relative to the portfolio size. Although it seems small, tight margins in the competitive lending market mean even slight fluctuations can impact profitability. The bank’s lending decisions become less informed, potentially leading to a misalignment between risk and return.

The Tension Between Provisions and Revenue

One of the key insights from this scenario is the direct tension between increasing loan provisions and protecting revenue. As the model degrades, the bank’s risk assessment becomes less reliable, leading to an increase in loan loss provisions by £100,000—a 1% rise relative to the existing £10 million reserve. This adjustment is the bank’s way of cushioning itself against higher default risks due to less accurate risk predictions.

However, the need to increase provisions often competes with the drive to maintain profitability. If the bank becomes too conservative, setting aside more for potential losses, it constrains the capital available for lending, which can further depress revenue. This balancing act is one of the more nuanced aspects of managing risk in a banking environment.

Importantly, the 1% increase in provisions relative to the loan reserve is more significant than the 0.25% revenue decline, indicating the bank prioritises caution over profitability as model accuracy declines. This can protect the bank in the short term but may limit growth if revenue generation continues to slide.

Regulatory Risk: The Bigger “What If”

Perhaps the most uncertain, but potentially significant, outcome from this scenario is the risk of additional regulatory oversight. As credit models degrade, there’s a chance that regulators will scrutinise the bank’s risk management practices more closely, leading to additional costs from audits, validations, and possible corrective measures. The probability of this intervention is modeled at 10%, with an expected cost of £125,000—a sum comparable to the revenue loss.

However, this cost could rise sharply with regulatory intervention, potentially reaching £2 million in a worst-case scenario. Such intervention might lead to enforced capital charges or costly actions like external model revalidation or portfolio restructuring.

Crucially, though, the likelihood of such regulatory action is low. The simulation places a 95% threshold for total financial impact at £600,000, which is well below the £1.5 million 1-in-200 scenario loss. This suggests that while regulatory risk is a concern, it remains more of a “tail risk”—unlikely, but costly if realised.

The Real Insight: It’s About Understanding The Risk

One of the key takeaways from this scenario is that the expected financial hit from losing the Credit Risk Modelling Team—£150,000 on average—is manageable, representing only a small percentage of the overall portfolio.

The real insight lies in how moderate impacts—steady revenue decline and slight provision increases—can compound over time. Moreover, this scenario highlights how the degradation of credit risk models has a ripple effect across revenue, provisions, and compliance. These aren’t isolated costs; they interact in complex ways that require a careful balancing act. For example:

Increasing loan provisions reduces the risk of future losses but at the cost of immediate profitability.

Pursuing higher-risk loans to compensate for lost revenue may backfire, increasing defaults and regulatory scrutiny.

Regulatory audits, while a low probability, could compound losses, especially if remedial actions are enforced.

Conclusion: Preparing for Understated Yet Meaningful Risks

While the loss of a Credit Risk Modelling Team doesn’t immediately spell disaster for a bank, the gradual degradation in model accuracy can lead to a series of small but meaningful financial impacts. These effects accumulate over time, putting pressure on the bank’s revenue, provisions, and compliance efforts.

The key lesson for risk managers is to recognise rare outcomes like regulatory intervention, but not to overlook how incremental degradation in operational capability can progressively undermine financial performance.

This type of analysis is particularly valuable in proactive risk management. For example, it can be leveraged as part of an Operating Model review, ensuring that key functions—like credit risk modeling—are adequately staffed and supported. It could also guide succession planning, identifying critical teams that need robust contingency plans to avoid operational disruptions.

In summary, this kind of scenario-based modeling not only helps quantify the potential risks of team loss but also serves as a strategic tool for workforce and operational planning, helping firms safeguard themselves against impacts that might otherwise go unnoticed.

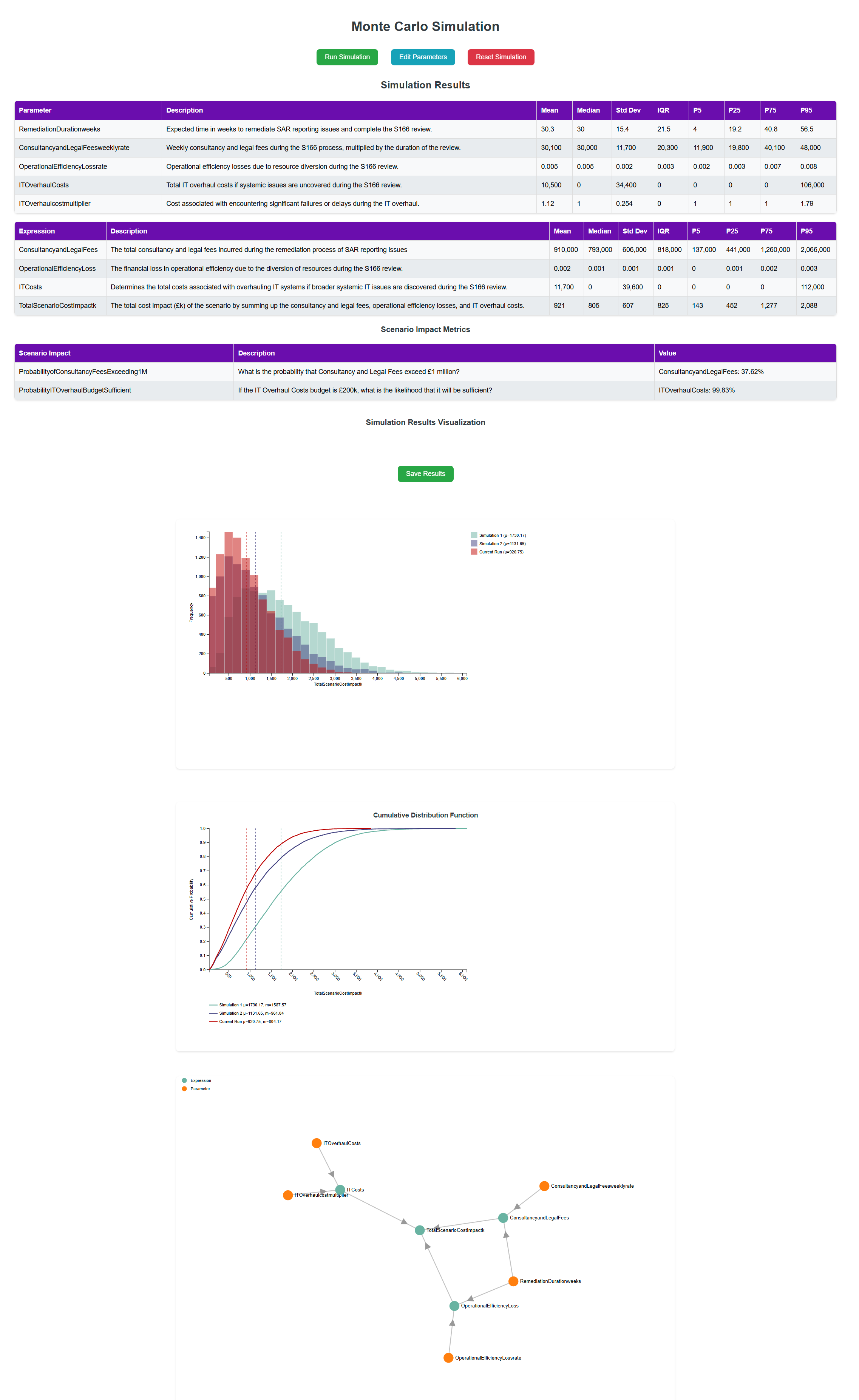

In today’s regulatory landscape, financial institutions are expected to maintain airtight compliance processes, especially when it comes to critical reports like Suspicious Activity Reports (SARs) required under anti-money laundering (AML) regulations. However, as demonstrated by recent simulations, even slight lapses in data aggregation or internal communication can lead to significant regulatory consequences. In this article, we will explore an operational risk scenario where Monte Carlo simulations shed light on the potential fallout of incomplete SAR filings. We’ll look at how this advanced risk modeling technique helps institutions prepare for the unexpected and mitigate costly risks.

Understanding the Scenario: Incomplete SARs and Regulatory Fallout

Imagine a bank that operates across various divisions—retail, high-net-worth (HNW) individuals, and treasury. Each of these divisions generates transaction data that needs to be aggregated and analyzed to detect suspicious activity. But what happens when the system responsible for aggregating this data misses certain high-risk patterns?

In this scenario, faulty data aggregation and miscommunication between the IT and compliance teams led to SARs being filed with incomplete information. While the IT team had identified the issue, the problem was never escalated to the compliance team, who continued to submit these incomplete reports. A regulatory audit, such as an S166 review by the Financial Conduct Authority (FCA), later revealed this critical failure.

Key Insights from the Monte Carlo Simulation

Monte Carlo simulations are invaluable tools for understanding how these operational failures can impact an institution. The dataset modeled several parameters to predict the cost and duration of remediation, potential efficiency losses, and the likelihood of uncovering deeper systemic issues. Here are the significant takeaways:

Remediation Duration: The simulation showed a remediation timeline ranging from 12 to 78 weeks, with an average of 26 weeks, depending on the severity of the failure. This wide range reflects the uncertainty in resolving such complex IT and communication issues.

Cost Implications: Weekly consultancy and legal fees during the review were estimated between £10,000 and £50,000, with a mean of £20,000. Over the course of a potential 26-week remediation period, this could add up to nearly £500,000. The possibility of an IT overhaul—should systemic issues be discovered—could drive costs even higher, reaching a mean estimate of £1,000,000, with a 20% likelihood of overruns adding an additional 50%.

Operational Efficiency Loss: During the remediation process, the bank could face operational efficiency losses between 0.017% and 0.083%, small percentages that could nonetheless impact profitability over the long term. These losses stem from the diversion of resources towards resolving the regulatory breach rather than focusing on core business operations.

Systemic IT Issues: There’s a 30% chance that the S166 review could uncover broader systemic IT issues, requiring a significant overhaul. This introduces additional layers of risk, both in terms of operational disruptions and unexpected financial costs.

Breaking Down the Cost Drivers: Key Expressions in the Simulation

The Monte Carlo simulation provides a powerful lens through which to examine how various factors combine to determine the overall financial impact of this operational risk event. Below are the key expressions that model the event’s cost dynamics.

Consultancy and Legal Fees Formula: Consultancy and Legal Fees weekly rate * Remediation Duration weeks Mean value: £1.6 million (range: up to £3.1 million) Key Insight: The S166 review is anticiplated to last around 51 weeks, and the weekly cost is modeled at a mean rate of £31,000. In a 1-in-20 scenario, this cost could reach £3.1 million. The length of the review significantly influences the financial impact.

Operational Efficiency Loss Formula: (Operational Efficiency Loss rate / 100) * Company revenue * Remediation Duration weeks Mean value: £760,000 (range: up to £1.6 million) Key Insight: A minor operational efficiency loss during the review has a significant impact on the bottom line. At a rate of 0.5% (mean) of the bank’s £300 million annual revenue, this loss accumulates to around £760,000. In a 1-in-20 scenario, where losses peak at 0.8%, the total efficiency loss could rise to £1.6 million. Small inefficiencies, when compounded over time, can create significant financial stress.

IT Overhaul Costs Formula: IT Overhaul Costs * IT Overhaul cost multiplier Mean value: £230,000 (range: up to £1.6 million) Key Insight: If systemic IT issues are uncovered during the review, the overhaul could be costly. Because of the considerable uncertainty around IT overhaul costs, we introduced the multiplier, which suggests costs could rise by nearly 80% and could exceed £1.6 million.

Total Scenario Cost Impact Formula: Consultancy and Legal Fees + Operational Efficiency Loss + IT Overhaul Costs Mean value: £2.5 million (range: up to £4.8 million) Key Insight: Combining all the cost elements, the total scenario cost impact averages around £2.5 million. In a 1-in-20 event, this figure could rise to £4.8 million, showing the importance of preparing for low-probability but high-impact operational events.

The Power of Simulation: Small Efficiency Losses, Big Financial Impact

One of the most striking results of this simulation is how a seemingly small operational efficiency loss—modeled at a rate of 0.5%—translates into substantial financial consequences. This finding underscores the hidden costs of operational disruptions. For a company that processes millions of transactions and generates significant annual revenue, small inefficiencies compound rapidly over time, draining profits that would otherwise be reinvested into growth or innovation.

The IT Overhaul Cost Multiplier: Amplifying Financial Risk

Another key variable in the scenario is the IT overhaul cost multiplier, which introduces a layer of uncertainty around the potential expenses tied to IT failures. This multiplier reflects the likelihood that unanticipated technical difficulties or delays will drive up costs beyond initial estimates.

What’s particularly important about the multiplier is its amplifying effect on uncertainty. The base cost assumption is already significant, but the potential for it to double in the event of IT failures makes this a critical area of focus for further evaluation.

Real-World Implications for Financial Institutions

This scenario also emphasizes the importance of proactive risk management. Identifying potential system failures early, improving communication between IT and compliance teams, and investing in robust IT infrastructures are all strategies that can mitigate the risk of costly regulatory reviews and operational inefficiencies.

The findings underscore the ripple effect that overlooked errors in compliance reporting can have on a financial institution. A remediation process that takes upwards of a year, coupled with escalating consultancy fees and potential systemic IT issues, can lead to significant operational and financial strain.

More importantly, the Monte Carlo simulation helps quantify these risks, providing management with a clearer view of the potential costs and timelines involved. This empowers decision-makers to prioritize resources effectively, reduce inefficiencies, and ensure that their compliance frameworks are robust enough to avoid such regulatory pitfalls.

The Broader Context: A Growing Need for Advanced Risk Management

Monte Carlo simulations, long a staple in financial modeling for market risk, are now proving their value in operational risk as well. Beyond the financial services sector, industries such as manufacturing and logistics are also adopting these techniques to optimize their risk management strategies, demonstrating the versatility and growing relevance of simulation-based approaches.

Adopting a data-driven scenario approach can provide the foresight needed to navigate complex environments and avoid costly oversights. Whether you are in financial services or another industry, now is the time to integrate simulation-based approaches into your operational risk management strategy.

Closing Thoughts: In an era where compliance missteps can cost millions and undermine a firm’s reputation, leveraging Monte Carlo simulations can mean the difference between reactive firefighting and proactive risk mitigation. Are you ready to take your risk management to the next level?

System Crash, Compliance Risk, and Financial Fallout

In the interconnected world of financial services, operational disruptions can quickly cascade into compliance breaches, reputational damage, and substantial financial loss. Consider a scenario where a key third-party provider responsible for anti-money laundering (AML) transaction monitoring experiences a system outage. This results in a prolonged downtime, forcing the bank to review transactions over £2,000 through a semi-automatic in-house process, while transactions exceeding £10,000 are blocked for manual review.

While manual processing may serve as a temporary workaround, it introduces significant operational strain and the risk of errors. Worse yet, failure to detect suspicious activity or failure to correctly processing transactions could potentially lead to fines or reputational harm. To quantify this risk, we ran a Monte Carlo simulation that models potential outcomes based on key parameters such as downtime duration, transaction volume, and manual error rates. The results shed light on the depth of the problem and the financial exposure that such an outage could create for the bank.

Key Findings from the Simulation: Navigating the Risks of AML Downtime

Imagine it’s midday, and your bank’s third-party anti-money laundering (AML) system suddenly crashes. At first, this seems manageable thanks to robust continuity planning. The bank has a proportional, risk-based approach: transactions below £2,000 continue to be processed normally, with a post-event review in place to identify any suspicious activity. Transactions over £2,000 are routed through a semi-automatic in-house system, while those exceeding £10,000 are sent for manual review. The response helps, but as the outage stretches into a 36-hour downtime, the backlogs grow, mistakes happen and the the pressure intensifies.

1. Downtime and Transaction Volumes: A Growing Backlog

At first, the downtime seems manageable. The average modeled downtime is 6 hours, but in more severe cases, it could last up to 18 hours or even 37 hours. As each hour passes, the number of transactions requiring AML review builds up.

Under normal conditions, the bank processes 200 transactions per hour. In a severe but plausible 36-hour outage scenario, the simulation suggests an average of 160 transactions over £2,000 will need semi-automatic processing and in an extreme event – such as an extended outage in the run up to a national holiday – this number could climb to 660 transactions. Meanwhile, while the simulation suggests on average there will be 31 high-value transactions sent for manual review, this number could rise to 140 transactions in extreme situations.

As these high-value transactions wait for manual review, customers grow impatient. Each delay compounds the risk of compensation claims and customer dissatisfaction.

2. Compensation Costs: How Delays Add Up

Every delayed transaction carries a potential compensation cost. For mid-range transactions between £2,000 and £10,000, the bank expects to pay £100 goodwill for each delayed transaction. For high-value transactions exceeding £10,000, the compensation rises to £500 per transaction.

The simulation estimates that, on average, the compensation for mid-range transactions will amount to £13,000, however this could surge to £54,000. When high-value transactions are added to the mix, compensation costs increase further. On average, these would add £16,000 to the total, but in a worst-case scenario, this could climb to £66,000. Altogether, the total compensation costs could range from £29,000 on average, up to £120,000 in a worst-case scenario. These costs, while significant, only tell part of the story.

3. Manual Errors: An Unseen Risk

As the bank turns to manual processes, another risk emerges: human error. The base assumption is that 5% of manually processed transactions will contain errors, but under pressure, this figure could rise to 7% or more.

The simulation shows that, on average, the bank could make errors in the processing of 14 transactions resulting in an additional £3,300 in additional compensation costs. However, in a worst-case scenario, with high volumes and a higher error rate, manual errors could cost the bank up to £25,000. These errors aren’t just financially costly—they further strain operational resources and damage client trust.

4. Worst-Case Scenario: When Everything Goes Wrong

As it turns out, the simulation suggests the event will be around 6 hours in duration, impacting around 160 customers, requiring £32,000 to be paid in compensation. However, the extreme 1-in-200 scenario, the downtime drags on, more transactions are delayed, manual errors spike, and compensation claims stack up. In this scenario, the bank would have to compensate 1,200 customers including additional payments for errors to 98 of those customers, with an expected compensation bill of £140,000. Even in a severe yet plausible 1-in-20 scenario, the compensation could still reach £87,000.

Beyond the financial impact, the reputational risk looms large. High-value clients might tolerate a short delay, but extended downtime—especially when coupled with errors—could lead to long-term damage to the bank’s customer relationships. And on top of all this, the response of the regulator could be significant.

Bringing It All Together: The Broader Implications of Downtime

The narrative that emerges from this simulation isn’t just about compensation—it’s about operational vulnerability and gaining insight into our risk tolerance and thresholds. A system crash may seem like a technical glitch, but as this scenario shows, the financial and reputational risks escalate rapidly. Even with semi-automatic systems and manual reviews in place, prolonged downtime amplifies costs, frustrates customers, and risks compliance breaches.

Monte Carlo simulations give us a way to anticipate these risks, providing a clear picture of how different scenarios play out. For a bank relying on third-party services for critical AML monitoring, understanding the worst-case scenarios is essential to avoid the financial and reputational fallout.

In today’s fast-moving world, data-driven risk management is no longer optional. Firms must embrace these tools to assess operational resilience and protect against the unexpected.

Strengthen Your Operational Resilience with Simulation-Based Risk Management

In light of these findings, Risk functions should take proactive steps to incorporate Monte Carlo simulations into their operational risk management frameworks. Understanding the potential range of outcomes, from best-case to worst-case scenarios, enables better decision-making and more effective resource allocation during a crisis.

If your organisation relies on third-party services for critical functions such as AML monitoring, now is the time to evaluate your disaster recovery and business continuity plans. How well-prepared are you for a similar outage? How can simulation-based tools help quantify and mitigate these risks?

By adopting simulation-based approaches, financial institutions can better manage the complexities of operational risk and ensure they are prepared for the unexpected. In today’s uncertain world, it’s not just about managing what you know—it’s about preparing for what you don’t.

The future of risk management lies in data-driven simulations. It’s time to harness their power to secure your organisation’s financial and operational future.

Mitigating Rogue Trading with Governance, Controls, and Reporting Systems

In the corridors of high finance, certain traders stand out not just for their skills. These individuals often occupy pivotal positions within their firms, granting them access to sensitive information and significant trading power. Under pressure to deliver consistent profits, their actions are rarely overt; instead, they weave a web of small deceitful decisions that go unnoticed until the damage is irreparable.

The environment in which these traders work is typically one of intense pressure and high expectations, where success is measured by short-term gains and personal reward. Employers, driven by the demand for impressive performance, may inadvertently create fertile ground for reckless behavior by prioritising results over strict compliance. Ultimately, it is a combination of personal ambition, a permissive corporate culture, and the ability to operate undetected for a period of time that makes these traders uniquely risky assets for their employers.

In the world of financial trading, rogue trading remains a significant operational risk, often leading to catastrophic losses when left unchecked. As financial institutions continue to grow in complexity and trading environments evolve, mitigating these risks requires robust governance, enhanced internal controls, and effective reporting systems. In this follow-up article, we explore the practical steps that organizations can implement to reduce the likelihood of rogue trading and mitigate its impact, based on established regulatory guidelines and operational risk management frameworks.

The Root Causes of Rogue Trading

Rogue trading often arises when unauthorized trades bypass internal controls, leverage is misused, or trading operations are poorly monitored. The infamous case at Société Générale in 2008, where a rogue trader caused billions in losses, highlighted the potential for disaster when governance mechanisms and risk controls fail. Key factors contributing to rogue trading incidents include:

Lack of oversight and governance at senior levels

Inadequate separation of duties between the front, middle, and back offices

Weak internal control mechanisms

Ineffective reporting and early-warning systems

To mitigate these risks, financial institutions must adopt a comprehensive approach that integrates robust governance structures, stringent control measures, and real-time reporting mechanisms.

Key Mitigation Strategies

While Monte Carlo simulation provides valuable insights, it functions as one component of a comprehensive control framework:

Primary Controls

Secondary Controls

Real-time position monitoring and reconciliation

Four-eyes approval processes for trades

Independent price verification

Automated limit checks

Scenario analysis and stress testing

Monte Carlo simulation for exposure assessment

Independent risk appetite monitoring and control assurance

Robust risk and audit oversight

The simulation results should inform the calibration of these controls. For example, if simulations show potential for rapid loss escalation under certain conditions, institutions might:

Control

Description

Independent risk oversight

Establish an independent risk management function to provide oversight and challenge on risk-taking activities.

Lower position limits

Reduce the maximum positions that traders can hold to limit the potential for outsized losses.

Increase margin requirements

Require traders to post higher levels of margin to cover their positions, reducing the leverage in the system.

Enhance monitoring frequency

Increase the frequency of position monitoring and reconciliation to identify potential issues more quickly.

Implement additional approval layers for specific product types

Introduce additional layers of approval and oversight for complex or higher-risk products.

1. Strengthening Governance Mechanisms

At the heart of effective risk management lies strong governance. Senior management must have a full understanding of both the potential and actual operational risks posed by market-related activities, particularly within trading desks. Governance measures should ensure:

Clear segregation of duties between the front office (trading), middle office (risk management), and back office (settlements and accounting). This separation helps prevent unauthorized actions by ensuring that no one individual has control over the full trade lifecycle.

Committees with risk oversight roles should be established. These committees must have adequate resources to challenge front-office activities and ensure that any suspicious trading behavior is addressed immediately.

Promotion of a risk-aware culture within the trading environment is also critical. Traders should operate under clear terms of reference, with frequent reviews and escalation procedures in place to investigate breaches of trading limits.

Governance frameworks that promote transparency, accountability, and high professional standards in trading environments provide a critical first line of defense against rogue activities.

2. Enhancing Internal Controls

Robust internal controls are essential for detecting and preventing unauthorized trading activities. Institutions should implement the following controls across all trading desks:

Rigorous trade confirmation, reconciliation, and settlement processes: All trades should be immediately reported and confirmed by the middle or back office, ensuring that any discrepancies are identified early. Confirmation processes should occur independently of the front office to reduce the risk of manipulation.

Mandatory “desk holidays” for traders: Requiring traders to take at least two consecutive weeks away from their desk annually allows a fresh set of eyes to review their books, making it harder for fraudulent behavior to go undetected.

Real-time monitoring of leverage and credit limits: Since rogue trading often involves excessive leverage, institutions should implement real-time systems to track positions and prevent breaches of set limits. Large trades or deviations from normal trading patterns should trigger automatic alerts for immediate investigation.

Additionally, audit trails documenting every step of a transaction—from initiation to settlement—enable institutions to maintain transparency and accountability, ensuring that even minor errors are traceable and correctable.

3. Improving Reporting and Early-Warning Systems

Early detection of rogue trading relies heavily on effective reporting systems. Institutions must establish internal reporting structures that can identify and escalate material incidents quickly:

Comprehensive risk reporting systems should generate real-time alerts when trading patterns deviate from expected norms. Whistle-blowing mechanisms should also be in place to allow staff to report suspicious behavior without fear of retribution.

Daily profit and loss (P&L) and position reconciliations: These reconciliations are critical for spotting unusual spikes or anomalies in trading activities, which may indicate rogue behavior. Random checks on trades, combined with analysis of key risk indicators, allow for rapid intervention before losses accumulate.

Regular fraud testing and scenario analysis: Institutions should periodically test their systems for vulnerabilities to fraud and rogue trading. By conducting scenario analyses, organizations can better understand where and how fraudulent behavior might emerge, enabling them to adjust their controls accordingly.

Moreover, reports should be well-structured, clear, and escalate issues in real-time to relevant control functions and senior management, ensuring that corrective action is taken swiftly.

Fraud Prevention and Detection: A Critical Element

Given the complexity of modern financial markets, the potential for both internal and external fraud has risen sharply. Institutions must actively integrate fraud detection into their operational risk frameworks. This can be achieved by:

Developing a fraud risk mapping program: By mapping potential fraud risks within trading activities, institutions can better prepare their systems to detect anomalies.

Increased fraud awareness training for all staff involved in trading and settlements. This ensures that individuals at every level understand their role in preventing and reporting fraudulent activity.

Rigorous testing and monitoring of fraud prevention systems, ensuring that they can handle the scale and complexity of modern trading environments.

Conclusion: Building Resilience Against Rogue Trading

Mitigating the risks associated with rogue trading requires more than just compliance with basic regulations—it demands a proactive, integrated approach that encompasses governance, controls, and reporting systems. Monte Carlo simulations can help quantify potential exposures, but real-time governance and control mechanisms are essential for preventing these exposures from materializing into actual losses.

Financial institutions must prioritize the development of a risk-aware culture, enforce clear segregation of duties, and leverage advanced technology to detect and respond to anomalies in trading activities. By doing so, they can reduce the likelihood of rogue trading incidents and limit their impact if they do occur.

In an industry where operational risks are ever-evolving, institutions that strengthen their internal frameworks are better positioned to protect both their reputations and their bottom lines.

Operational risk in financial institutions can emerge from unexpected corners, with one of the most severe examples being rogue trading. A single unauthorized trade can spiral into catastrophic losses, especially when factors like market volatility and leverage come into play. In this context, Monte Carlo simulation proves to be an invaluable tool, offering insights into potential risks, helping institutions prepare for worst-case scenarios, and making informed decisions to mitigate these risks.

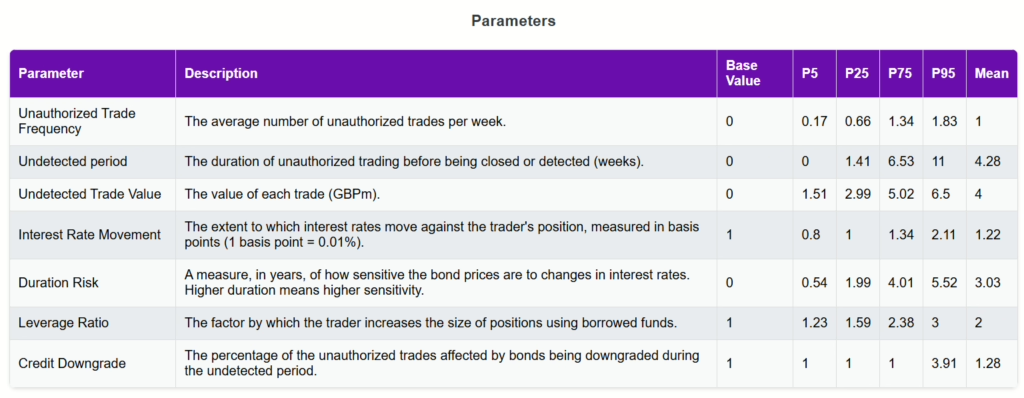

In this article, we explore how Monte Carlo simulation can help financial institutions quantify and manage the risks associated with rogue trading, using a real-world scenario focused on unauthorized bond trading at a mid-sized UK bank.

The Rogue Trading Scenario: Complex Risks with Severe Consequences

In this scenario, a rogue trader on a fixed-income desk engages in unauthorized bond trading, taking highly leveraged positions. The situation worsens when adverse interest rate movements, credit downgrades, and forced liquidation lead to escalating losses. This underscores the critical role of risk oversight and the devastating impact of hidden exposures.

But how can institutions foresee such complex risk dynamics? This is where Monte Carlo simulations become crucial. By modeling a wide range of possible outcomes—factoring in trade frequency, undetected periods, interest rate shocks, and market responses—Monte Carlo allows risk managers to quantify potential losses and develop strategies to address them.

How Monte Carlo Simulation Supports Decision-Making

Capturing the Full Spectrum of Risk

In rogue trading scenarios, many factors influence potential losses, from how long unauthorized trades remain undetected to the size of interest rate shocks and credit downgrades. Monte Carlo simulation captures the variability across these dimensions, generating thousands of possible outcomes based on different combinations of these variables. This gives decision-makers a clearer picture of not just the likely outcomes but also the extreme cases that could lead to severe financial exposure.

For instance, the simulation models key parameters such as:

The frequency of unauthorized trades.

The undetected trading period.

Interest rate shifts and their impact on bond prices.

Leverage ratios, which amplify both gains and losses.

The possibility of credit downgrades affecting bond positions.

By integrating these variables, the simulation provides a holistic view of the potential exposure, from common scenarios to rare, catastrophic losses.

Quantifying Rare but High-Impact Events

One of the greatest benefits of Monte Carlo simulation is its ability to help businesses prepare for extreme but rare events. In the rogue trading scenario, adverse events such as interest rate shocks and credit downgrades have low probabilities but can lead to substantial losses when they do occur. The simulation quantifies these tail risks, giving risk managers data on how severe the impact could be in a 1-in-20 or 1-in-200 scenario.

For example, if interest rates shift by an unexpected margin, the simulation shows the effect on unauthorized leveraged bond positions. The outcomes from this simulation provide answers to critical questions: How much could we lose in a worst-case interest rate shift?What happens if a significant portion of unauthorized trades are downgraded in credit quality?

By offering probabilities attached to these extreme scenarios, Monte Carlo simulation gives institutions the foresight to prepare for the unexpected.

Understanding the Impact of Leverage

In financial markets, leverage is a double-edged sword—it magnifies gains but also amplifies losses. In this scenario, the rogue trader’s use of leverage multiplies the potential damage from unauthorized trades. The Monte Carlo simulation helps quantify just how much leverage could increase exposure to loss. It models different leverage ratios and shows how each increment could escalate financial risk, particularly in combination with market events like interest rate shifts or credit downgrades.

Through the simulation, institutions can see the compounded effects of leverage, making it easier to set limits or design policies to restrict unauthorized leverage usage. This is crucial because excessive leverage often turns what might have been a manageable loss into a disaster.

Measuring Combined Risk Exposures

Rogue trading risk doesn’t stem from a single factor—it’s a combination of market events (such as interest rate movements and yield curve shifts) and internal missteps (like undetected trades and excessive leverage). Monte Carlo simulation enables institutions to measure combined exposures by calculating how these various factors interact.

For instance, in this rogue trader scenario, the simulation evaluates:

The effect of leveraged unauthorized trades on exposure.

The impact of interest rate changes on those leveraged positions.

Additional risks from yield curve shifts and credit downgrades.

The simulation also accounts for convexity adjustments—an additional cost incurred when unwinding bond positions in illiquid markets. All of these combined exposures can lead to total losses that are much larger than initially expected. By modeling these interactions, the Monte Carlo simulation reveals the potential for severe losses beyond what simple risk metrics might suggest.

Preparing for Regulatory and Market-Based Metrics

Finally, Monte Carlo simulations can inform regulatory stress testing by showing if an institution’s total exposure breaches critical thresholds under extreme conditions. For example, in this scenario, the simulation tracks whether exposure exceeds £12 million in a 1-in-20 event or £30 million in a 1-in-200 event—key metrics that would trigger regulatory or market-based concerns. This insight helps financial institutions comply with stress testing requirements while also giving them the opportunity to adjust their risk management strategies proactively.

Conclusion: Monte Carlo Simulation as a Strategic Risk Management Tool

In scenarios like rogue trading, where the interplay of unauthorized activity, market volatility, and leverage creates a web of risk, Monte Carlo simulation provides a clear framework for navigating uncertainty. By generating a range of possible outcomes, this tool helps financial institutions quantify both common and extreme risks, supporting data-driven decision-making that mitigates potential losses.

As financial markets become more complex and interconnected, the importance of understanding and managing operational risks cannot be overstated. Whether facing rogue traders or market shocks, Monte Carlo simulations offer a critical lens through which institutions can prepare for the worst while optimizing their strategies for the best outcomes.

Incorporating such simulations into your operational risk management approach today could be the key to avoiding tomorrow’s financial disaster.